Alaska for Sale:

The Carbon Dump, the Credit Harvest, and the $2 Billion Federal Subsidy Hidden Inside an LNG Bill

How the governor pitched clean hydrogen to Japan for four years, asked the legislature to vote on a gas pipeline, and enabled a private developer to capture more than $2 billion annually in 45Q and 45V federal tax credits from Alaska’s geology, while the state receives $2.50 a ton and permanent geological liability in return.

What the Governor Said in Japan and What He Asked the Legislature to Vote On

In June 2022, Governor Mike Dunleavy concluded a trade mission to Japan and told reporters that Alaska could supply Japan with natural gas and clean hydrogen for decades to come. He traveled with the Alaska Gasline Development Corporation. His meetings covered LNG, blue hydrogen, and ammonia. That same month, the AGDC submitted a concept paper to the United States Department of Energy seeking $850 million in federal hydrogen hub funding, describing a facility at the Nikiski terminal capable of producing more than 500,000 metric tonnes of qualifying clean hydrogen per year using North Slope natural gas as feedstock.

In December 2022, the governor published an op-ed on RealClearEnergy titled ‘Alaska’s Map to Clean Hydrogen Leadership.’ He wrote that natural gas is a key ingredient for hydrogen production, that increasing global demand for low-carbon hydrogen is fueling progress for Alaska LNG, and that Alaska is well positioned to compete because of its geology suited for carbon capture. The op-ed was hosted on the AGDC website.

In April 2024, the Biden White House Japan State Dinner fact sheet committed the United States to exploring cross-border carbon dioxide transport and storage hubs between Alaska and Japan. The Alaska Department of Natural Resources presented that fact sheet as a featured slide in its own legislative testimony to the House Finance Committee the same month.

In March 2025, Governor Dunleavy concluded a trade mission through Taiwan, Thailand, South Korea, and Japan traveling with the heads of AGDC and Glenfarne Group. The pitch included LNG, clean hydrogen, and carbon management.

On May 27, 2026, the first day of the Alaska Legislature’s special session on the AKLNG pipeline, the governor’s retained energy consultant Nicholas Fulford of GaffneyCline told the Senate Finance Committee that gas is not the driver of the project’s economics. He declined to name the actual driver. No legislator asked what it was.

This paper names it.

The 45Q Architecture: $85 a Ton to the Operator, $2.50 a Ton to Alaska

The Gas Treatment Plant at the north end of the AKLNG pipeline is projected to cost $10.9 billion. Its primary function, as described in the Department of Revenue’s own benefit analysis, is to extract carbon dioxide from the raw North Slope gas stream and sequester it in subsurface formations, ensuring eligibility for federal 45Q tax credits. The DOR’s benefit analysis states those credits flow to the midstream GTP operator as non-taxable cash payments.

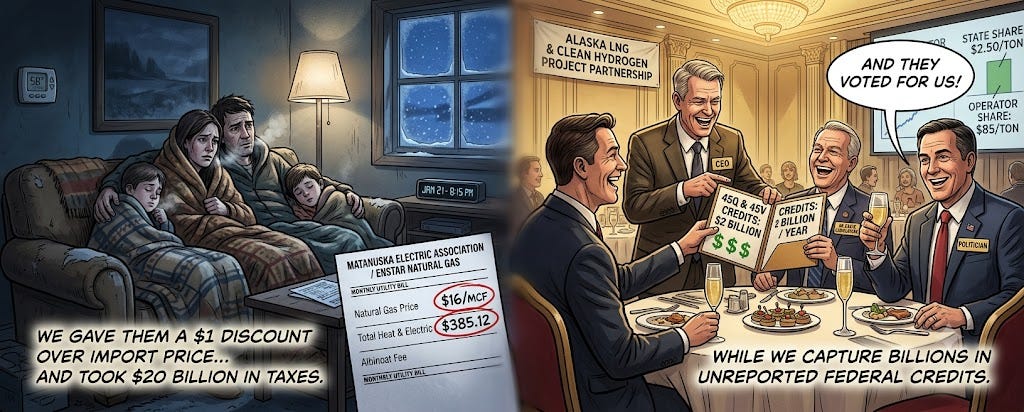

GaffneyCline’s May 27 Senate Finance presentation quantified the 45Q credit value precisely: 7 million tonnes of CO2 at $85 per tonne equals $595 million per year, for twelve years. That figure represents the single largest annual revenue stream associated with the GTP, exceeding the LNG export tariff contribution to the operator’s revenue at base-case gas prices.

Alaska’s return on that activity, under HB 50 passed in 2024, is $2.50 per tonne in injection royalties. The operator collects $85. Alaska collects $2.50. The ratio is 34 to 1, flowing entirely in the operator’s direction, from Alaska’s geology, under a regulatory framework Alaska built at its own expense.

HB 50 also, critically, enabled the import of foreign industrial carbon dioxide for injection into Alaska’s geology. The DNR’s April 2024 legislative presentation described the cross-border CO2 transport opportunity using the White House Japan State Dinner commitment and a Wall Street Journal report on specialized CO2 carrier vessels being built for delivery to Alaska. Under the framework as enacted, Alaska’s ground becomes the permanent waste repository for the industrial emissions of economies Alaska sold its energy to, at $2.50 per ton, while the operator collects federal credits for storing them.

Source: DOR HB 381 Benefit Analysis, March 25, 2026; GaffneyCline SFIN Presentation, May 27, 2026; HB 50 enrolled text, AS 31.25 et seq.; DNR HFIN Presentation, April 22, 2024; White House Japan State Dinner Fact Sheet, April 10, 2024.

The 45V Architecture: $1.5 Billion a Year That Has Never Appeared in a Fiscal Note

The Section 45V Clean Hydrogen Production Credit pays up to $3 per kilogram of qualifying clean hydrogen produced, for ten years, to projects that begin construction before the statutory deadline. At the AGDC’s stated production volume of 500,000 metric tonnes of clean hydrogen per year at the Nikiski terminal, that credit generates $1.5 billion annually. Analysis by University of Alaska Fairbanks and energy researchers confirms that calculation at the stated production scale.

The production process is Steam Methane Reforming of North Slope natural gas. The CO2 byproduct is captured and sequestered in Cook Inlet reservoirs under HB 50’s Class VI injection framework, qualifying the hydrogen production for the maximum 45V credit tier. The pipeline delivers the feedstock gas. The GTP conditions it. The Nikiski terminal produces the hydrogen. Each stage requires the preceding one. The pipeline is not incidentally associated with the hydrogen credit. It is the physical delivery mechanism for the feedstock without which the credit does not exist.

The One Big Beautiful Bill Act, signed into federal law in July 2025, moved the 45V construction commencement deadline to December 31, 2027. SB 2001’s construction trigger is January 1, 2028. Those two dates are aligned. The urgency argument driving the special session’s 30-day timeline is not driven by LNG market competition from Canada. It is driven by an IRS credit deadline. That deadline has not been named on the floor of either chamber or in any committee hearing during the special session.

No fiscal note before the Alaska Legislature during either the regular session or the special session quantifies the 45V credit stream. No amendment has required disclosure of the credit transfer partners who would receive the 45Q and 45V credits through the IRS Section 6418 transferability mechanism. The legislature has been asked to authorize the largest tax abatement in Alaska’s history for a project whose primary economic driver has never appeared in a fiscal note.

Source: IRC Section 45V; One Big Beautiful Bill Act, July 2025; AGDC DOE Hydrogen Hub Concept Paper, November 2022; UAF and energy researcher analysis published in Must Read Alaska, June 2026; SB 2001 enrolled text, Section construction trigger.

The World’s Carbon Dump: Foreign Waste, Seismic Geology, and a Trust Fund That Runs Out in 12 Years

The Cook Inlet basin is not a passive geological container. The DNR’s own February 2023 legislative presentation described it accurately: seismic activity, numerous folds and faults. The Castle Mountain Fault runs through the Mat-Su Borough. USGS research documents it as the only fault in Southcentral Alaska with both historical seismicity and Holocene surface rupture, meaning it has broken the surface in geologically recent time and carries a documented slip potential approaching 2 meters in a single event. A magnitude 6.0 earthquake struck approximately 30 to 40 miles from Anchorage on Thanksgiving Day 2025, consistent with the ongoing compressive seismic regime the USGS has characterized for this basin.

The proposed primary storage formation, the Beluga River gas field, is a fault-propagation fold structure built on a steeply dipping reverse fault. Peer-reviewed literature on CO2 injection-induced seismicity is direct: fault systems with complex activation mechanisms make the evaluation, prediction, and control of injection-induced seismicity extremely difficult. Oklahoma’s geology is far less tectonically active than Cook Inlet. Saltwater disposal injection there still produced a five to ten-fold increase in measured seismicity.

Cook Inlet has been drilled since the late 1950s. Hundreds of wellbores penetrate the proposed storage formations, many cemented under standards that predate modern supercritical CO2 exposure requirements. Each one is a potential migration pathway. The EPA’s Class VI permitting framework requires operators to identify and assess every penetrating well within the area of review. In a basin with 38 documented gas fields and 10 oil fields, that requirement has significant cost implications that appear in no fiscal note associated with HB 50.

The trust fund HB 50 established to cover long-term monitoring costs stops collecting contributions after 12 years of injection. The CO2 remains underground indefinitely. Permanent monitoring liability transfers to Alaska taxpayers after a 50-year post-injection period with no hard cost cap. The legislature built a permanent house on a rented foundation and handed the deed to the state upon departure of the tenant.

Source: USGS Holocene Slip Rate publication, Castle Mountain Fault western segment; USGS Cook Inlet basin characterization; ScienceDirect CO2 injection-induced seismicity review, 2023; HB 50 enrolled text, trust fund provisions; DNR HRES Presentation, February 2023.

What Alaska Surrendered: $20 Billion in Taxes, Near-Import-Parity Gas, and No Share of the Credits

The Department of Revenue’s own analysis of the proposed legislation is precise. The governor’s tax restructuring cuts expected state revenue by $7 billion through 2063. Municipalities lose another $13 billion during the same period. The combined $20 billion in surrendered revenue is what the Alternative Volumetric Tax replaces. The total project AVT projected through 2062 across all jurisdictions, state and municipal combined, is $2.594 billion, approximately $86 million per year averaged across 30 years of operations.

The Municipal Advisory Group, a body of state and local officials who negotiated with the project’s prior sponsors including ExxonMobil, BP, and ConocoPhillips, reached agreement on payments in lieu of taxes totaling $628 million per year for municipalities alone, plus $800 million in construction-phase impact payments. The current legislation produces $86 million per year for all government recipients combined. That comparison has not been presented to the legislature as a single document in any committee hearing.

Glenfarne proposed a gas price to Alaska utilities of $16 per thousand cubic feet on June 3, 2026. The Department of Revenue’s own estimate of imported LNG cost in 2033 is approximately $17 per thousand cubic feet. The tax abatement being offered in exchange for a $1 per thousand cubic feet improvement over import parity is worth approximately $20 billion in surrendered government revenue over the project’s life.

No provision in any bill before the legislature gives Alaska a contractual share of the 45Q or 45V credit revenues. No provision requires the operator to pass any portion of the credit revenues through as a reduction to the in-state gas tariff. No provision establishes a revenue floor tied to the project’s actual economic drivers. The legislature is being asked to legislate the tax structure for a project whose primary revenue streams flow entirely outside Alaska’s reach.

Source: DOR HB 381 Benefit Analysis, March 25, 2026; AVT document, DOR; SB 2001 fiscal note, May 20, 2026; Alaska Beacon, June 4, 2026; DOR HFIN Presentation, May 22, 2026.

The Leverage Alaska Held and Did Not Use

The 45Q credit requires Alaska’s pore space, leased under HB 50 at $2.50 per ton. Without HB 50 and the Class VI primacy framework the AOGCC sought, the GTP cannot qualify for 45Q credits regardless of where it is built. The 45V credit requires North Slope gas delivered by the pipeline to a terminal producing qualifying hydrogen. Without the pipeline, there is no 45V credit stream. Without Alaska’s gas resource, there is no feedstock. Without Alaska’s geology, there is no sequestration. The developer is not bringing an independent revenue-generating asset to Alaska. The developer is building a credit-capture platform on Alaska’s resources, Alaska’s geology, and a regulatory framework Alaska constructed and funded.

The correct negotiating posture, supported by every comparable global LNG framework in the GaffneyCline comparison table presented to the legislature, is to require a contractual share of the credit revenues as a condition of the tax concession. Nigeria holds 49 percent equity in Nigeria LNG. Qatar Energy holds a direct ownership stake in every LNG train at Ras Laffan. Papua New Guinea required full integrated project economics before concessions were granted. Every jurisdiction in GaffneyCline’s own global benchmark received either direct equity participation, a revenue floor, a domestic market obligation at regulated prices, or some combination.

Alaska received none of those. The $5 per thousand cubic feet Senate gas price cap was rejected by Glenfarne. The $12 per thousand cubic feet construction-phase cap was rejected by Glenfarne. The municipal equity ownership option was removed from the House bill before passage. The one negotiating instrument that would have tied Alaska’s return to the project’s actual revenue driver, a contractual share of the federal credit streams, was never proposed by any legislator in either session.

Source: GaffneyCline SFIN Presentation, May 27, 2026; GaffneyCline HRES written responses, April 17, 2026; HB 381 version G Summary of Changes; Alaska Beacon, June 5, 2026.

What the Constitutional Standard Requires

Article VIII, Section 2 of the Alaska Constitution states that the legislature shall provide for the utilization, development, and conservation of all natural resources belonging to the state, including land and waters, for the maximum benefit of its people. That standard is not aspirational language. It is the governing constitutional mandate every legislator swears to uphold.

Maximum benefit of its people requires that the full revenue picture, including the federal credit streams enabled by Alaska’s regulatory framework, be on the table before Alaska’s tax base is surrendered. It requires that the ratepayer benefit used as public justification for the tax abatement be contractually guaranteed at a price genuinely below import parity. It requires that Alaska’s permanent liabilities, geological storage under HB 50 and infrastructure rate risk under AKLNG, be matched by protections that extend at least as long as those liabilities.

The constitutional standard has been invoked repeatedly in floor statements, sponsor documents, and committee testimony during both sessions. The fiscal structure being enacted does not meet it. The primary vehicle for establishing it, a revenue floor tied to the project’s full economic architecture including the federal credits that are its actual driver, has not been introduced as an amendment by any member of either party in either session.

What Alaska Could Still Negotiate

The special session runs through June 19, 2026. No vote has been taken on SB 2001. The leverage Alaska holds is documented, specific, and quantifiable. If Alaska negotiated a 20 percent share of the combined 45Q and 45V credit stream, applying the standard partnership structure used in comparable global projects, the annual revenue to Alaska would exceed $400 million per year during the credit period. Applied to reduce the in-state gas tariff, that revenue share would bring the delivered gas price to Alaskan utilities below $4 per thousand cubic feet at base-case assumptions. Ratepayers would receive genuinely cheap gas. The state would receive a recurring revenue stream tied to the project’s actual economic engine. Glenfarne would retain 80 percent of a federal credit program it could not access without Alaska’s framework.

That negotiation has not happened. The $16 per thousand cubic feet proposal on the table produces a $1 per thousand cubic feet improvement over import parity in exchange for $20 billion in surrendered tax revenue and permanent geological liability. The constitutional standard requires Alaska to do better than that. The document record shows Alaska has the leverage to do so.

What You Can Do Before June 19

The Senate Finance Committee is still working. Contact your legislators directly at akleg.gov or call the legislative switchboard at 907-465-4648. Ask one question: where is the fiscal note that quantifies the 45Q and 45V credit streams flowing to the operator from Alaska’s geology?

If the answer is that no such fiscal note exists, that answer belongs on the record before any vote is taken.

Dana Raffaniello lives in Palmer, Alaska. He works as a network engineer, reads Alaska energy legislation closely, and publishes analysis of its fiscal and structural implications at raff6482.substack.com. He is running for the Mat-Su Borough Assembly, District 2. He has no commercial interest in any energy project discussed in this analysis. Primary sources for all claims are cited throughout.