The Carbon Credit Tab

The national debt just crossed 100 percent of GDP. Alaska's governor and legislature responded by making it easier for foreign companies to collect billions in federal carbon credits

The Number That Should Have Stopped Juneau Cold

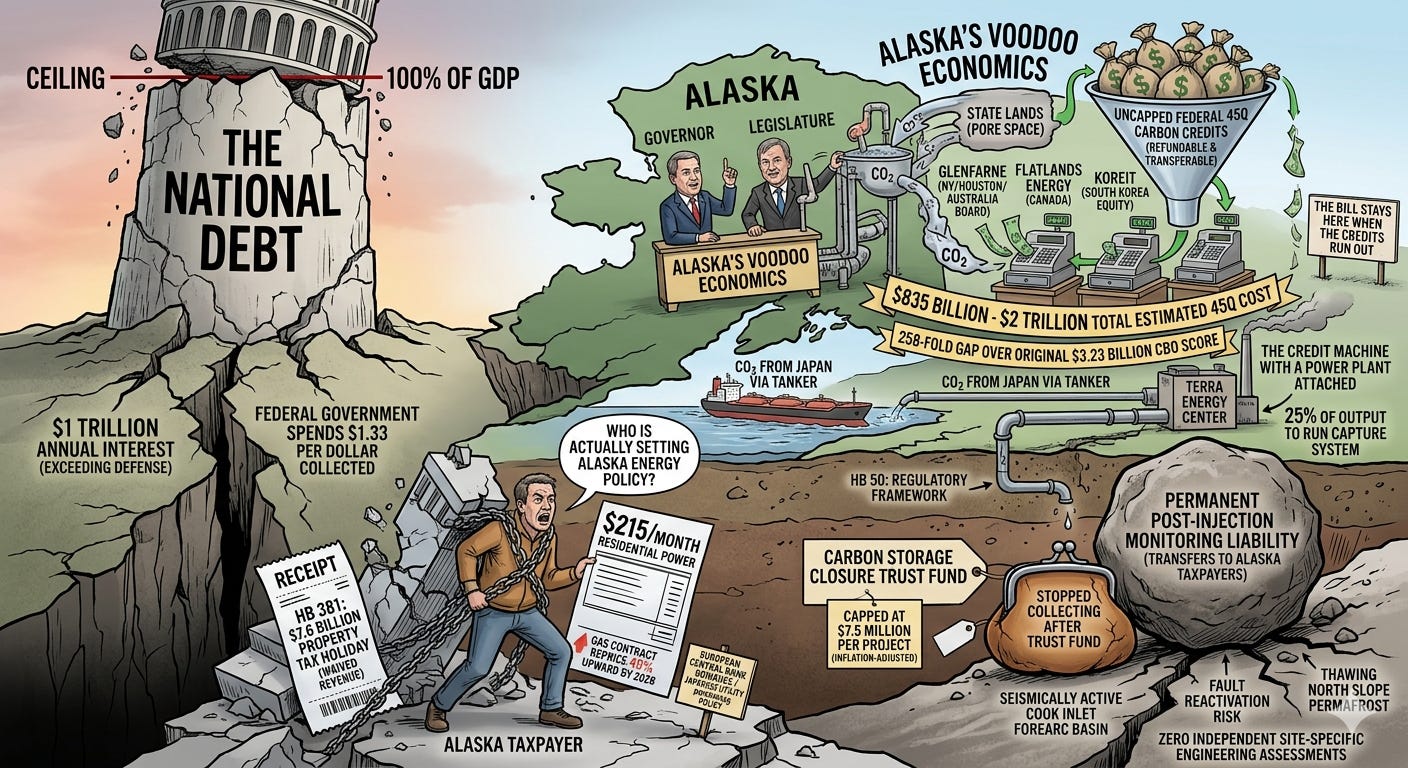

Last Thursday the Bureau of Economic Analysis released its first-quarter 2026 GDP estimate. Debt held by the public reached $31.27 trillion. Nominal GDP for the trailing twelve months came in at $31.22 trillion. The national debt is now larger than the entire U.S. economy, debt-to-GDP at 100.2 percent, a threshold that has been crossed only twice before in American history.

The first time was brief and mechanical: the pandemic that hit in 2020 temporarily collapsed GDP while spending surged, pushing the ratio over 100 percent for a few quarters before the economy recovered. The second time was real and earned: the end of World War II, when the country had fielded sixteen million service members, built a two-ocean Navy, and spent years defeating two industrialized military powers on opposite sides of the globe. The debt accumulated then was paid down to 34 percent of GDP within two decades because the spending created something durable, the national purpose was defined, and the underlying economic activity was real.

What is driving it now deserves a harder look.

The federal government is spending $1.33 for every dollar it collects. Interest payments on the accumulated debt hit $1 trillion this year for the first time in American history, surpassing what the country spends on national defense. The Congressional Budget Office projects that interest costs will rise from $1 trillion this year to $2.1 trillion by 2036, eventually becoming the single largest item in the federal budget, exceeding Medicare, exceeding Medicaid, exceeding the entire defense establishment.

Inside that trajectory sits a single tax credit program whose original CBO score was $3.23 billion over ten years. The credit is Section 45Q of the Internal Revenue Code, the Credit for Carbon Oxide Sequestration. Independent analysts now project its total cost at $835 billion, with estimates ranging to $2 trillion if the credit window is extended and enhanced. That is a 258-fold gap between what Congress was told when it created the program and what it is now projected to deliver to private companies. The program is uncapped. The credits are refundable, meaning the Treasury cuts checks to companies regardless of their tax liability. They are transferable, meaning they can be sold to third parties. They run for twelve years per project. And the sequestration volumes they are paid on are self-reported, because the EPA is simultaneously proposing to eliminate the independent federal verification infrastructure that was supposed to catch fraud.

The Inspector General for Tax Administration examined 45Q claims from 2010 to 2019. Ten taxpayers had claimed over $1 billion in credits. Credits worth $894 million did not comply with EPA reporting requirements. The companies had insufficiently documented whether the carbon they claimed credit for remained underground. This was not a fringe program with marginal problems. This was 99 percent of all 45Q credits claimed, and $894 million of them were noncompliant.

Congress preserved and extended 45Q in the most recent reconciliation package. The One Big Beautiful Bill kept the credit intact on a federal balance sheet at 100.2 percent of GDP, paying $1.33 per dollar of revenue, with interest costs exceeding defense spending for the first time in the nation’s history.

Against that balance sheet, Alaska’s governor and legislature spent the 2026 session making it easier for foreign companies to access those credits. The mechanism they built is a layered subsidy architecture spanning three bills, two geological formations, a permanent monitoring liability backed by only $7.5 million in financial assurance per project, and a property tax holiday worth $7.6 billion in foregone state and local revenue. The 45Q credits that load-bear the entire structure are paid by federal taxpayers on a sovereign balance sheet now larger than the economy backing it.

This is where that money goes and who it goes to.

HB 50: The Foundation

The governor introduced HB 50 in January 2023 as part of a four-bill Carbon Management and Monetization package. The bill that became law built Alaska’s carbon storage regulatory framework from the ground up: Class VI well permitting authority, pore space leasing on state lands, long-term monitoring obligations, and the Carbon Storage Closure Trust Fund.

The trust fund is where the liability structure reveals itself. Storage operators pay a surcharge into a project-specific account for the first twelve years of injection, totaling $7.5 million per project adjusted for inflation. The surcharge then stops. The CO2 stays underground permanently. After a minimum of fifty years of post-injection monitoring, the operator can apply for a certificate of completion. When that certificate issues, the state assumes permanent responsibility for monitoring and maintenance. The enrolled bill text is explicit: if the trust fund balance is insufficient to cover monitoring costs, the state is not liable for damages. Alaska taxpayers carry the remainder with no statutory ceiling on their exposure.

A storage operator collects federal 45Q credits for twelve years. The trust fund collects surcharges for twelve years. Then both stop. The monitoring obligation does not stop. It is permanent, beginning roughly sixty years after the first surcharge payment, funded by whatever inflation-adjusted fraction of $7.5 million remains at that point.

When the bill reached the Senate floor, one senator called the tree credit provisions embedded in it a scam, then voted yes. The final tally was 37 to 3 in the House and 18 to 2 in the Senate. Those margins look like consensus. They reflect what happens when potential revenue is discussed and liability structure is not.

The stated urgency for passing the law was not Alaska’s energy needs. It was the 45Q credit deadline. DNR’s own sponsor statement said so: federal 45Q tax credits are enhancing the economics of CCUS projects, and protracted project timelines necessitate prompt action. The federal subsidy clock, not Alaska’s power supply gap, drove the legislation.

Who Actually Required This

Before getting to what HB 381 and SB 280 do on top of HB 50, it is worth asking a prior question: where did the requirement for carbon credentialing actually come from?

It did not come from Alaskans. It did not come from Railbelt ratepayers who need firm baseload generation. It came from the European Central Bank’s supervisory framework for climate and environmental risk, which European institutional investors passed downstream to energy companies as a condition of capital access, which Japanese utilities organized into formal carbon-neutral LNG purchasing alliances as a condition of long-term purchase commitments.

The bill’s most vocal legislative defender acknowledged this plainly during the public exchange that produced the most detailed technical record in the legislative history of this issue. Buyers and investors expect a plan for CO2, he said, whether we like it or not. That is an accurate description of who is actually setting Alaska energy policy. The European Central Bank issued supervisory guidance. European institutional capital required ESG compliance. Japanese utilities formed purchasing alliances conditioning LNG contracts on carbon credentialing. Glenfarne needed those purchase agreements and that European capital to finance the project. Therefore Glenfarne needed CCS. Therefore Alaska needed HB 50.

Alaska’s legislature built state law, permanent geological liability, and a twelve-year trust fund around the compliance requirements of European banking regulation and Japanese utility purchasing policy. Neither institution is accountable to Alaska voters. Neither will share the monitoring obligation when the trust fund runs dry.

A senior member of the Senate Finance Committee was more direct than anyone else in the entire legislative record. He said on the Senate floor during HB 50’s passage that Japan is studying Alaska as a CO2 storage site because their islands are too small. Cook Inlet, he said, is sitting in a prime location. He said it as though it were good news. The Hilcorp-Sumitomo-K Line feasibility study confirmed he meant it: a plan to ship liquefied CO2 from Japan across the Pacific in tanker vessels for permanent injection into Cook Inlet pore space, with a proposed storage capacity of 50 gigatons, equivalent to Japan’s CO2 emissions over fifty years.

Alaska’s pore space, regulated under HB 50, funded by a $7.5 million trust fund, with permanent monitoring liability transferring to Alaska taxpayers, is being actively studied as a permanent repository for Japanese industrial waste. The senator who announced this as a competitive advantage is the same senator who is currently endorsing the Alaska Center’s candidate for the Chugach Electric board.

HB 381 and SB 280: The Property Tax Holiday

HB 50 built the legal framework. HB 381 and SB 280 built the financial incentive layer on top of it.

These bills replace the existing 2 percent oil and gas property tax on the Alaska LNG project with an Alternative Volumetric Tax during a ramp-up period. The Department of Revenue’s own numbers show what that replacement costs. Under current law, the state would receive $8.4 billion in property taxes from the pipeline project by 2042. Under the governor’s proposal, $829 million. Local governments would receive $5.7 billion under current law, versus $728 million under the bill. That is a 90 percent reduction in state tax take and an 87 percent reduction in local tax take.

The definition of qualified property eligible for the tax holiday explicitly includes integrated carbon capture, utilization, and storage infrastructure. The CCS component gets the same holiday as the base pipeline, the gas treatment plant, and the liquefaction terminal. The billion-dollar appendage added to the project to satisfy European capital market ESG requirements is exempt from the property tax that would have applied to it.

The developer receiving this benefit is Glenfarne, which holds 75 percent of the project. That stake was awarded through a no-bid contract whose details have been kept from the legislature. Glenfarne is headquartered in New York and Houston with an Australian-dominated executive board and no prior LNG pipeline operating experience. It has refused to provide the legislature with its financial projections. The legislature is being asked to waive $7.6 billion in tax revenue based on a private company’s unverifiable assertion that the project will not proceed without relief, without any independent confirmation that the assertion is true.

On top of the property tax holiday, Glenfarne stands to collect up to $7 billion in federal 45Q carbon credits on the project. Those credits are paid from the federal Treasury, which is currently spending $1.33 per dollar of revenue collected, paying $1 trillion per year in interest on debt that has now crossed 100 percent of GDP.

Terra Energy Center: The Credit Machine With a Power Plant Attached

The Alaska LNG project is not the only 45Q architecture operating in Alaska right now. The University of Alaska Fairbanks produced a feasibility study of the proposed Terra Energy Center coal plant in the West Susitna drainage. The study’s own FAQ stated the essential fact plainly: a new biomass and coal-fired power plant for the Railbelt would probably not be an option for consideration without CCS, because capturing carbon dioxide earns tax credits of $85 per tonne sequestered.

Read that sentence carefully. The power plant exists to produce CO2 in sufficient volume to qualify for the 45Q credit. Strip the credit and the $1.3 billion CCS component has no standalone economic rationale. Strip the CCS component and by the project’s own documentation the power plant is not viable. The Railbelt needs firm baseload generation. What it is being offered is a credit-harvesting mechanism that also produces electricity after consuming roughly 25 percent of its own gross output to run the capture system.

The developer is Flatlands Energy, a Canadian company and subsidiary of Alaska Asia Clean Energy Corporation based in Alberta. The equity investor is KOREIT, a South Korean private equity firm, with a committed $500 million. Major equipment agreements run through Hyundai Heavy Industries. The DOE grant program Terra applied to for $400 million has since been made unavailable. The primary potential buyer for the electricity, Chugach Electric, has publicly refused to purchase coal-generated power. No power purchase agreement has been signed with any utility. No coal mine is operating. The proposed mine is not on the road system.

The Matanuska-Susitna Borough Assembly overrode a mayoral veto to partner with Terra in a joint international marketing effort. The resolution embedded support for the West Susitna Access Road alongside support for the power plant concept. The same organizations whose coordinated campaign just installed an endorsed director on MEA’s board oppose both the West Susitna Access Road and the coal plant. The board member’s stated approach to MEA’s supply problem is demand reduction through rate increases. MEA, the utility most likely to be asked to purchase the power, has no power purchase agreement with Terra.

The Geology Nobody Examined

HB 50’s regulatory framework applies to two distinct geological formations with two distinct and serious risk profiles. Neither received an independent site-specific engineering assessment in the public legislative record.

The Terra Energy Center proposes to inject captured CO2 into the Beluga River gas field, a fault-propagation fold in the Cook Inlet forearc basin, transported 60 miles by pipeline from the plant site. The Beluga field is a complex structure with steeply dipping reverse faults and stacked, discontinuous channel-belt sandstone beds that make CO2 plume migration difficult to predict or contain. The Castle Mountain Fault, the only fault in Southcentral Alaska documented with both historical seismicity and Holocene surface rupture, runs through the Mat-Su Borough with a slip rate of approximately 3 millimeters per year and single-event slip potential of nearly 2 meters. A magnitude 6.0 earthquake struck the Cook Inlet region on Thanksgiving Day 2025.

CO2 injected as a supercritical fluid at commercial scale into a fault-propagation fold adjacent to an active reverse fault system, in a seismically active forearc basin, for a minimum of decades, carries a specific and serious leakage risk through fault reactivation. That risk is not hypothetical. It is documented in the scientific literature on CO2 injection and caprock integrity. It does not appear in the HB 50 legislative record, the HFIN presentations, or the DNR sponsor materials.

The Alaska LNG Gas Treatment Plant on the North Slope proposes to strip CO2 from the raw gas stream and inject it into the North Slope subsurface. The North Slope has continuous permafrost ranging from 200 to 600 meters deep at Prudhoe Bay. That permafrost is documented to be thawing. Permafrost serves as both a boundary condition and a natural seal component for the formations beneath it. A caprock system that includes frozen ground as a structural element is a caprock system whose integrity is a function of a warming baseline that is already established and accelerating.

The word permafrost does not appear in the HB 50 CO2 storage potential discussion in any DNR presentation. The North Slope slide that describes storage potential lists low seismic activity and numerous folds and faults as characteristics. It does not mention the permafrost above the target formations or what happens to seal integrity as that permafrost thaws over the fifty-year post-injection monitoring period the law requires before a certificate of completion can even be considered.

Two injection sites. Two distinct geological risk categories. One $7.5 million trust fund per project. Zero independent site-specific engineering assessments in the public record.

The Federal Balance Sheet This All Sits On

The 45Q credit program began with a Congressional Budget Office score of $3.23 billion over ten years. The Treasury Department’s own estimate jumped from $20.1 billion in 2021 to $30.3 billion in 2022. Independent analysts now project $46 billion per year, with a total cost of $835 billion by 2042 and potentially $2 trillion if credit values are extended further. That projection is based on 142 announced projects. Glenfarne’s Alaska LNG project and Terra Energy Center are not yet in that count.

The Inspector General for Tax Administration found in 2020 that ten taxpayers claimed over $1 billion in 45Q credits from 2010 to 2019. Credits worth $894 million did not comply with EPA reporting requirements. The companies had insufficiently documented whether the carbon they claimed credit for remained underground. The IRS disallowed 59 percent of the noncompliant credits, worth approximately $531 million. No further update has been released since April 2020.

The EPA is now proposing to eliminate subpart RR reporting obligations, the federal mechanism designed to verify that CO2 actually stays underground. The interim fix is private third-party certification by independent engineers. The IRS requires claimants to maintain records for only three years. The credit window is twelve years. The storage obligation is permanent. At no point in this chain does a government inspector verify in the field that the CO2 being credited is actually underground and staying there.

Alaska receives approximately 45 percent of its state revenues from federal transfers, the highest federal dependency ratio in the nation. The FY2027 budget must draw $1.5 billion from the Constitutional Budget Reserve to balance, drawing down a savings account that currently holds roughly $3 billion. The state is simultaneously waiving $7.6 billion in property tax revenue for a foreign LNG developer, backing its permanent geological monitoring liability with only $7.5 million in trust fund assurance per project, and positioning its pore space as a repository for Japanese industrial CO2 shipped across the Pacific in tanker vessels.

All of it is financed by a federal government spending $1.33 per dollar collected, paying more in interest than it spends on defense, at 100.2 percent debt-to-GDP, on a 45Q program whose cost has grown 258 times beyond what Congress was told when it was created.

The Questions the Legislative Record Cannot Answer

What is the fully independent cost per delivered kilowatt-hour from the Terra Energy Center without the CCS system, without the 45Q credit, without the DOE grant, evaluated against the Railbelt load forecast through 2035?

What actuarial analysis determined that $7.5 million per project, collected over twelve years, is adequate to fund the permanent post-closure monitoring obligation that the state assumes after a minimum fifty-year post-injection period in a seismically active Cook Inlet basin or beneath documented thawing permafrost on the North Slope?

What independent geological assessment has been conducted of CO2 plume migration risk in the Beluga River fault-propagation fold under commercial-scale injection pressure, and what is the estimated probability of fault reactivation under those conditions given the Castle Mountain Fault system’s documented Holocene activity?

What commitment, if any, does Glenfarne’s confidential financial model show for the period after the twelve-year 45Q credit window closes, and what is MEA’s rate exposure if imported LNG becomes the primary Railbelt fuel source after the gas supply cliff arrives?

What is the legal mechanism by which Alaska’s geological monitoring liability is capped if the Carbon Storage Closure Trust Fund is exhausted before the post-closure monitoring obligation ends, given the enrolled bill text that says the state is not liable for damages if the fund is insufficient?

These questions were not asked in the legislative record. They have not been answered. The bills passed anyway.

What Can Actually Be Done

Contact Senators Murkowski and Sullivan and Representative Begich this week with one specific ask. Will they support HR 1946, the 45Q Repeal Act, a bipartisan bill introduced jointly by one of the House’s leading fiscal conservatives and a progressive California Democrat? If not, ask them to explain in writing how an uncapped federal tax credit program projected at $835 billion to $2 trillion is consistent with fiscal conservatism at 100.2 percent debt-to-GDP. A form letter response does not answer the question. Require a specific answer about a specific bill.

Demand four amendments to HB 381 before final passage. Exclude CCS infrastructure from the definition of qualified property eligible for the Alternative Volumetric Tax abatement, let it stand on its own economic merits. Condition any tax abatement on public disclosure of the developer’s complete financial model subject to legislative audit. Require binding long-term power or gas purchase agreements from creditworthy buyers before any abatement takes effect. Require a bond or insurance instrument covering the gap between the trust fund balance and the projected cost of 100 years of post-injection monitoring, calibrated by an independent actuary, as a condition of any Class VI permit issued under HB 50.

Amend HB 50’s trust fund structure. The injection surcharge should continue for as long as the state holds monitoring responsibility, not just for the twelve years the operator collects federal credits. Tie the collection window to the liability window. Anything less transfers open-ended geological liability to Alaska taxpayers without any financial floor beneath it.

Prohibit Alaska pore space from accepting foreign-origin CO2. One statutory sentence in HB 50 closes the Japan tanker plan permanently: pore space leased under this chapter may not be used for the storage of carbon dioxide captured outside the United States. This is not anti-development. It is basic sovereignty over a state resource that the Alaska Constitution directs be developed for the maximum benefit of Alaskans.

Commission the study that has never been funded. Direct the Alaska Energy Authority to produce an independent cost analysis of a modern coal plant fueled by Usibelli or Wishbone Hill coal, without carbon capture, evaluated against the Railbelt load forecast and the Cook Inlet gas repricing curve through 2035. This study does not exist because no developer will fund it without a federal credit to collect on the other end. The AEA can fund it directly. The legislature can direct it. The answer it produces belongs to MEA’s 58,000 members and Chugach’s 90,000 members before the gas cliff arrives.

The Closing Account

The national debt crossed 100 percent of GDP last Thursday. It has done that twice before: once in a pandemic that briefly shrank the economy, and once while building the military force that won the Second World War. The debt accumulated then was paid down to 34 percent of GDP within two decades because the spending created something durable and the national purpose was clear.

What the 45Q architecture creates is a twelve-year credit window, a permanent geological liability, a $7.5 million trust fund that stops collecting before the monitoring obligation starts, and a state regulatory framework designed around the compliance requirements of European banking regulation and Japanese utility ESG purchasing policy. The developer collecting the credits has an Australian executive board. The equity investor is a South Korean private equity firm. The feasibility study for the CO2 injection was conducted by a DOE contractor with an institutional interest in CCS commercialization. The legislative record contains no independent geological assessment of either injection site.

The governor signed HB 50. His administration built the regulatory framework. The Department of Revenue testified that the LNG project cannot proceed without property tax relief. The Alaska Gasline Development Corporation negotiated the no-bid arrangement. The legislature passed HB 50 at near-unanimous margins and is working through HB 381 and SB 280 now.

The people who will pay the tab are not in any of those offices. They are paying $215 a month for electricity in the third most expensive state in the nation for residential power, watching their gas contract reprice 49 percent upward by 2028, and waiting for a firm generation alternative that their cooperative board will not buy and their legislature has not honestly studied.

The credits will flow for twelve years. Then they will stop. The CO2 will stay in the ground. The state will monitor it permanently. The trust fund will have stopped collecting roughly forty years earlier.

That is the transaction Alaska just built.

Great article. Some additions:

We’re in an energy war and they want to burn 25% of our valuable resources to funnel US debt directly to Korean investors? That borders on SEDITION!

CO2 storage is never going to be permanent. It turns to carbonic acid with water. In Norway’s Snövit field, it’s lifting and fracturing 900’ of cap rock and escaping and migrating into formations never expected. That same carbonic acid carries heavy metals with it as well.

Side note: Geothermal projects do the same thing. They are hardly clean energy.

Side note two: Lisa Murkowski and Gene Peltola were met with and opened carbon credit trading LLCs when this legislation was being formulated. Nothing to see here eh?