The Development That Isn't

How Alaska's AKLNG Tax Legislation Accommodates a Federal Credit Collection Operation While Calling It Resource Policy

The fourth in a series on HB 50, the 45Q federal tax credit, and Alaska energy legislation

Alaska Is the Bank

There is a transaction worth describing plainly before it gets buried in the legislative record.

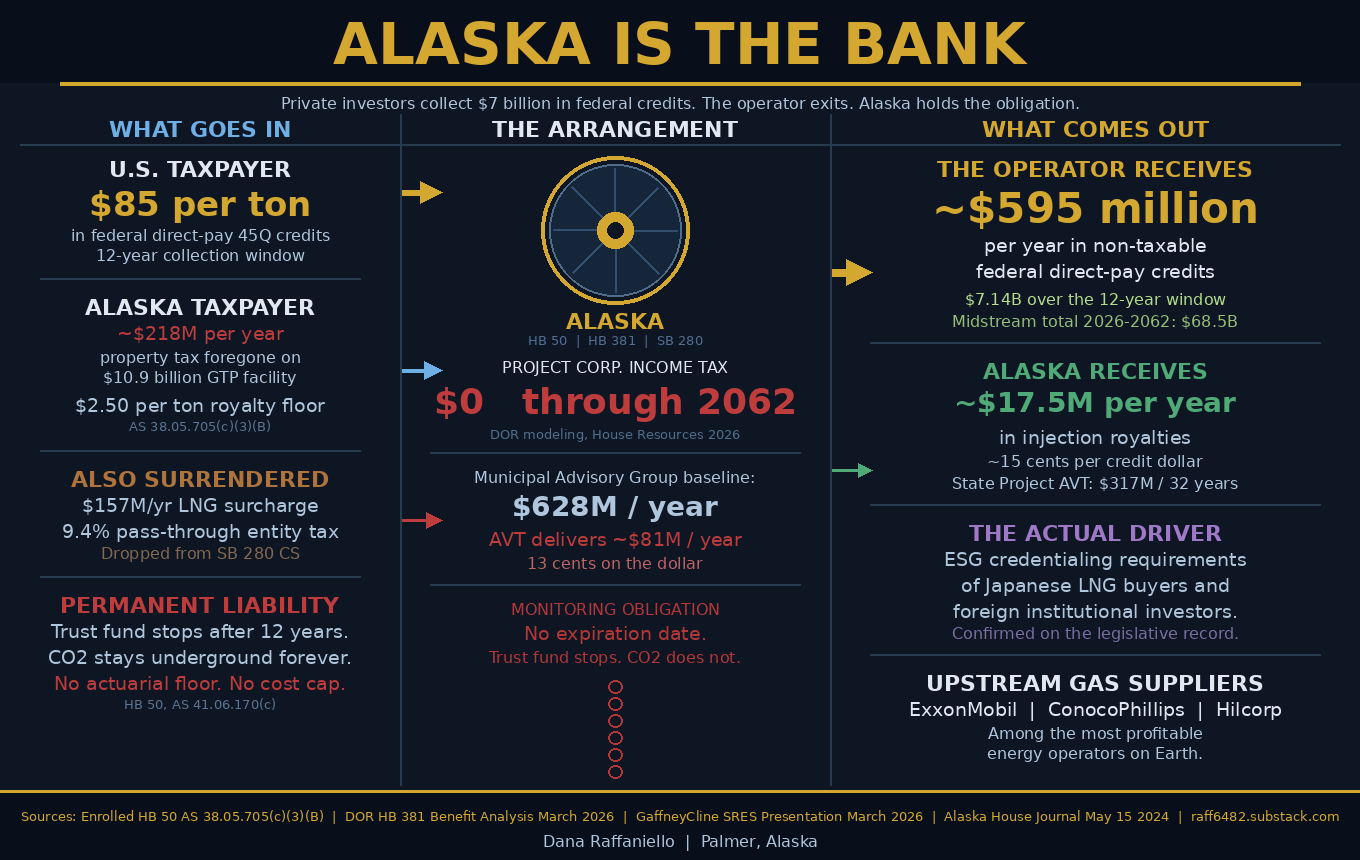

Private investors enter a carbon storage arrangement. They make deposits in the form of a 12-year surcharge that funds a closure trust account. They collect returns in the form of $85 per ton in federal direct-pay tax credits during the injection window. When the window closes, they exit. The CO2 stays underground. The monitoring obligation stays with Alaska taxpayers. The trust fund, whatever inflation has left of it after decades, is the only financial protection the state has against the cost of that obligation. The enrolled text of HB 50 states directly that if the fund is unavailable or insufficient, the state is not liable for damages. The liability is real regardless of what the fund contains.

That is the structure the Alaska Legislature put into statute in 2024. Two years later, the same legislature is advancing a pair of bills, HB 381 in the House and SB 280 in the Senate, that extend that structure by removing the property tax that would have been Alaska’s second lever in the arrangement. Supporters are calling this a development bill. They are calling it a free-market solution. They are saying capital goes where the numbers work and where the rules are clear.

Those numbers deserve a closer look, because they are in the public record.

The Development That Isn’t

Resource development in Alaska has always followed a recognizable pattern. The state owns the resource. A private operator extracts it. The state collects royalties and taxes on the extracted value. The operator profits from the sale. The resource is gone, but the revenue is real and the liability is bounded.

Carbon storage reverses that relationship at every step.

The resource being sold is not something extracted from the ground. It is the ground itself: the geological formation, the pore space, the capacity of the basin to hold injected CO2. The state does not receive royalties on extracted value because nothing is being extracted. It receives a per-ton injection fee starting at $2.50 under the enrolled statute. The operator does not profit primarily from what it sells to buyers. It profits from what the federal government pays it per ton of CO2 it injects, which is $85 per ton under current law, structured as a direct-pay cash refund available for the first 12 years of injection.

And the liability is not bounded. It is permanent.

The Gas Treatment Plant proposed for the North Slope as part of the Alaska LNG project is valued at $10.9 billion in the Department of Revenue’s own modeling. It is designed to remove CO2 from the raw gas stream, which is a function any LNG project requires, and then inject that CO2 underground rather than venting it. That additional step is what generates the 45Q credit. GaffneyCline, the consulting firm presenting to Senate Resources this session, confirmed the relationship directly: CO2 removal is essential to bring gas quality to LNG specification, and a CO2 removal plant is always present in the LNG value chain. The 45Q credit is the financial return on the added step of underground injection.

At 7 million tons of CO2 injected annually at $85 per ton, the Gas Treatment Plant generates approximately $595 million per year in federal direct-pay credits to the project operator. Over the 12-year credit window, that is roughly $7.14 billion flowing from the federal treasury to the operator for using Alaska’s geology.

Alaska’s share of that arrangement, under HB 50 as enacted, is $2.50 per ton in injection royalties. Approximately $17.5 million per year. The Department of Revenue’s own benefit analysis for HB 381 confirms what the state receives in state corporate income tax from the project operator: zero through 2042, zero through 2052, zero through 2062. The credits are structured as non-taxable cash payments at the midstream level. Alaska law explicitly bars adoption of 45Q credits by reference for state corporate income tax. The DOR built that assumption into its baseline model as a starting condition, not a variable.

The Gas Treatment Plant is a $10.9 billion facility. It generates $595 million per year for the operator. It generates $17.5 million per year for Alaska. It generates zero in state corporate income tax by design. That is not a development arrangement on Alaska’s terms. That is a credit capture operation built into Alaska’s statutory framework.

How Alaska Legislated Its Way Out of Revenue

Three bills across two legislative sessions created this arrangement.

HB 50, signed in 2024, created the legal authority for commercial carbon storage on state land. Before HB 50, there was no permitted framework for CO2 injection in Alaska, no lease structure, no pore space licensing, and therefore no foundation for a private operator to qualify for 45Q credits on Alaska geology. HB 50 provided all of that. The royalty floor was set at $2.50 per ton. That figure had been raised to $10 per ton in the Senate Finance committee substitute, but a floor amendment offered on the final day of the session deleted the higher figure and inserted $2.50. The amendment was adopted by unanimous consent. The enrolled statute, Chapter 23 SLA 2024, reflects that change at AS 38.05.705(c)(3)(B). That is the law as enacted.

The liability transfer structure was also established in HB 50: 12 years of surcharge collection, then the obligation passes to Alaska taxpayers indefinitely. The bill passed the House on its original third reading 32 to 8. On the final day of session, after the Senate had attached geothermal expansion provisions, Cook Inlet gas storage regulation, Cook Inlet reserve-based lending, and LNG import facility changes, the House voted on concurrence 37 to 3. Eight members who voted no on the substantive carbon storage bill found themselves voting on a package that had been expanded to include provisions many of them had separately supported. The carbon storage framework was unchanged. The additions were new.

HB 381 in the House and SB 280 in the Senate, both introduced in 2026, propose to replace the 20-mill property tax on the Gas Treatment Plant, pipeline, and LNG terminal with a volumetric tax calibrated to gas throughput. The Gas Treatment Plant at $10.9 billion assessed value would generate approximately $218 million per year under current property tax law. The Alternative Volumetric Tax replaces that with a rate calibrated to Mcf of gas, not to tons of CO2 injected. The facility that generates its revenue in tons of CO2 will be taxed in Mcf of gas. Those are two different meters measuring two different activities, and the one the legislature chose to write into law is the one that does not track the facility’s actual economics.

The total project AVT to all governments combined is projected at approximately $2.594 billion over 32 years of operation in the DOR’s own modeling, or roughly $81 million per year on average. The Municipal Advisory Group had previously negotiated a payment-in-lieu-of-taxes framework for this project at $628 million per year across all governments. The AVT replaces that benchmark with approximately 13 cents on the dollar.

SB 275, introduced as a standalone transparency and accountability bill, would have added a $0.15 per thousand cubic feet surcharge on gas processed into LNG, worth approximately $157 million per year to the state, and a 9.4 percent pass-through entity tax on pipeline-related LLCs and S-corps that currently pay zero state corporate income tax. Both provisions were stripped when Senate Resources absorbed most of SB 275 into the SB 280 committee substitute. Alaska got the governance paperwork from SB 275. The revenue provisions did not survive.

The DOR’s cashflow table for the full Alaska LNG project through 2062 shows midstream owners collecting $68.5 billion. State revenues over the same period total $22.5 billion, almost entirely from gas royalties and production taxes on upstream extraction from fields operated by companies including ExxonMobil, ConocoPhillips, and Hilcorp. Project corporate income tax for the midstream: zero.

And Into Permanent Liability

The liability that HB 50 built into statute does not appear in the revenue projections used to justify HB 381.

The DOR benefit analysis filed with House Resources this session projects $22.5 billion in state benefits from the Alaska LNG project over 32 years. It does not include the HB 50 injection royalties, which are accounted for under separate statutory authority. It does not include any accounting for the permanent monitoring obligation Alaska assumes after the 50-year post-injection period. It does not net out the foregone property tax revenue against the AVT that replaces it. It is denominated in nominal future dollars over a 32-year horizon, and the DOR acknowledges that production tax revenue in particular is highly uncertain due to oil price variability and upstream cost estimates.

The $22.5 billion headline figure is dominated by gas royalties and production taxes on upstream extraction. Those revenues flow from the value of the North Slope gas resource. They would accrue under any pipeline configuration capable of moving that gas to market. They are not compensation for the carbon storage framework or the property tax concession. They are the value of the gas itself, attributed to legislation whose central question is whether Alaska captures adequate value from the specific infrastructure being subsidized.

What Alaska receives specifically from the carbon storage operation: $17.5 million per year in HB 50 injection royalties, and a Gas Treatment Plant AVT that under HB 381 flows entirely to the North Slope Borough with zero to the state. Under SB 280’s committee substitute, the state receives 50 percent of the GTP AVT, approximately $90 million per year at full development. Together, Alaska’s state-level return from the operation generating $595 million annually in federal credits is in the range of 15 cents on every dollar of credit value collected for use of Alaska’s geology.

The liability outlasts the revenue. A legislator who voted for the bill and then acknowledged the trust fund concern in print subsequently said he would be shocked if any changes were made because not enough people consider it a problem. The number of people currently paying attention to a liability does not change whether the liability is real. It changes whether anything gets done about it before it lands.

Who the Numbers Actually Work For

The phrase repeated across public advocacy for this legislation is that capital goes where the numbers work and where the rules are clear.

The numbers do work. They work for the operator. The operator collects approximately $595 million per year in non-taxable federal cash from the Gas Treatment Plant. It pays $2.50 per ton in royalties on that credit-generating activity. It pays zero state corporate income tax on the midstream operation by statutory design. It benefits from a property tax replaced by a volumetric rate calibrated to gas throughput rather than to the injection activity that drives the facility’s economics. And after 12 years, when the credit window closes and the injection surcharge stops, the long-term monitoring obligation for CO2 stored in a seismically active Cook Inlet basin passes to Alaska taxpayers with no actuarial floor and no hard cost cap written into the statute.

It is worth being clear about who the upstream producers delivering gas to this facility are. GaffneyCline identified them directly in its Senate Resources presentation: potentially including ExxonMobil, ConocoPhillips, and Hilcorp. These are among the most profitable energy operators in the world. ExxonMobil holds 36 percent of Prudhoe Bay and 62 percent of Point Thomson. ConocoPhillips holds 36.5 percent of Prudhoe Bay and operates Kuparuk and Alpine. Hilcorp is the state’s largest oil field operator, averaging 135,000 barrels per day of North Slope production in 2024. The argument that this collection of companies needs a federal credit architecture and a state property tax concession to justify developing their North Slope gas does not hold up against their own financial statements. What those concessions do is make Alaska a more attractive host for credit collection by removing the fiscal friction that might otherwise have given the state negotiating leverage.

When a piece of legislation is described as necessary to attract private capital, the natural follow-on question is what that capital does once attracted. Here the answer is in the DOR’s own documents. The midstream owners collect $68.5 billion through 2062. The mechanism for that collection was built in three legislative steps. HB 50 gave them the geology. HB 381 and SB 280 give them the property tax concession. Alaska law gives them the corporate income tax shield. The federal credit program gives them $85 per ton. Calling that sequence resource development is not wrong in a technical sense. Resources are involved. But development in Alaska has always meant that when private operators extract value from Alaska’s land and resources, Alaska receives a meaningful share. These bills produce the opposite result.

On Reading the Documents

One thing worth saying plainly before the closing questions. Some of the public advocacy for this legislation has rested on figures that do not match the enrolled statute, characterizations of bill provisions that do not match the bill text, and voting histories that do not match the House Journal. These are not small gaps. When the case for a multi-billion-dollar tax concession is built on the committee substitute rather than the law that actually passed, or on a description of what a borough gets from a bill that does not give that borough what is claimed, the question worth asking is not just whether the policy is sound. It is whether the people advocating for it have read the documents they are citing.

Enrolled statutes are public. House Journals are public. DOR modeling is filed with the committee and published online. If the source material is too extensive to read carefully, that is a reasonable limitation to acknowledge. What it is not is a reasonable basis for correcting people who did read it.

The same standard applies to the underlying policy. Energy legislation that runs to dozens of sections across three separate bills is not understandable at the committee-substitute level. It requires reading the enrolled text, the DOR modeling assumptions, the GaffneyCline revenue analysis, and the allocation tables that show which government gets what from which facility component. If those documents are not being read, the gaps show up in public. They showed up here.

Questions the Record Raises

If the Gas Treatment Plant generates approximately $595 million per year in federal direct-pay credits, and the Alternative Volumetric Tax is calibrated to gas throughput rather than to tons of CO2 injected, on what basis is the tax rate set at a level that protects Alaska’s fiscal interest in that facility?

If the DOR’s own benefit analysis shows zero project corporate income tax through 2062, and Alaska law explicitly bars state adoption of 45Q credits for tax purposes, what is the statutory mechanism by which Alaska captures any share of the credit stream generated on its own geology?

If the Municipal Advisory Group previously negotiated payments in lieu of taxes at $628 million per year, and the AVT replaces that framework at approximately $81 million per year on average, what public analysis was presented to the legislature quantifying what local governments give up under this substitution?

If the carbon storage closure trust fund stops collecting after 12 years and the monitoring obligation does not stop, what actuarial determination has been made that the fund will be adequate for the obligation it is meant to cover?

If the answer to any of these questions is that not enough people currently consider it a problem, the follow-on question is: whose problem does it become when the credit window closes, the surcharge stops, and the CO2 remains underground on Alaska’s permanent geological account?

Alaska is the bank. The investors make deposits, collect returns, and exit. The liability stays. The question the legislature has not answered is what Alaska gets from that arrangement that it could not have gotten by negotiating on its own terms from the beginning.

Dana Raffaniello

Palmer, Alaska

Not affiliated with any commercial interest in the Alaska LNG project or any competing energy development.